The Efficiency Ratio Problem No One Is Actually Solving

Article

The Efficiency Ratio Problem No One Is Actually Solving

Every year, we attend banking conferences and hear advice echoed from stage after stage: “Get your data together to use AI.” It’s become a mantra in the industry. Everyone agrees it’s important, and then most go home and nothing meaningfully changes.

Data matters. And the leaders I talk to know it matters. The part that many miss today is understanding what “getting your data together” really means. That gap, between the slogan and the substance, is good news. It means the biggest opportunity to improve your efficiency ratio is still in front of you.

The Advice Everyone Gives but Nobody Finishes

When most people talk about getting your data together, they mean integration. Pull it from your core, your loan origination system, your CRM, your general ledger, and get it into one place, maybe a dashboard. Consolidated reporting is better than fragmented reporting, but if the end goal is using artificial intelligence to drive your efficiency ratio, then integration is step two of a ten-step journey.

The good news? The next steps are clearer than you might think.

What “getting your data together” really means is something far more granular and far more valuable. It means refining your data. It means embedding business context, encoding the business logic of your specific bank. It means having your data ready to use AI. Once you understand that distinction, the path forward becomes surprisingly actionable.

What Is a Data Foundation, Really?

A properly built data foundation is the unlock to using AI. It’s the key to doing the work you already do, but quicker, easier, and smarter.

Context matters because an LLM is extraordinary at processing language, identifying patterns, and generating output. What it cannot do, on its own, is understand that when your bank says, “Primary Relationship” or “Class 3 commercial real estate,” it means something slightly different than when the institution next door says the same thing. It doesn’t know your policy exceptions, committee preferences, or the dozen small decisions your best banker makes without even thinking about them.

That’s business logic. And every bank’s logic is different, which is a strength. Your institutional knowledge is a competitive asset. The data foundation doesn’t just store your data. It teaches AI how your bank actually works, preserving and scaling the expertise your team has built over years.

The Credit Memo Example

Take credit memo writing. It’s the example that illustrates the opportunity clearly, and once you see it, the same pattern shows up across the institution.

A credit memo is a structured synthesis of financial data, borrower history, market context, policy compliance, and risk assessment. It’s organized in a way that tells a clear story to a credit committee. It requires knowledge, context, and consistency.

A commercial banker and credit analyst might spend hours on a single credit memo. Not because the intellectual work is that complex, but because the assembly is. Pulling data from multiple systems, cross-referencing financials, ensuring the narrative aligns with current policy, formatting it correctly, reviewing it for completeness. Your bankers shouldn’t be spending their best hours on assembly.

Now the exciting question: what is stopping AI from writing that credit memo?

Frontier LLMs can synthesize, analyze, and write at extraordinary levels. What’s stopping them is context and business logic. The AI doesn’t know your bank’s specific credit policy. It doesn’t know how your committee likes to see deals presented. It doesn’t know that your chief credit officer always wants to see the debt service coverage calculated a certain way, or that your institution has a specific appetite for owner-occupied CRE that differs from the industry norm.

But if you’ve built the data foundation, if you’ve done the important work of refining your data, embedding your context, and encoding your logic, then an AI agent can draft that memo in your format, with your logic. The commercial banker reviews it, applies judgment, and moves on to the next relationship. The work that took hours now takes minutes. Multiply that across your team, across your branches, across a year, and you’re looking at a meaningful shift in your efficiency ratio from a single AI capability: writing credit memos.

A Framework for Doing This

So what does this look like in practice? I’d suggest a framework that starts with the work, rather than the tech.

Decompose. Pick a role: commercial banker, credit analyst, branch manager, compliance officer. Map the activities that role performs. Be specific. Instead of “lending,” think “spreading financials from tax returns.” Instead of “compliance,” think “reviewing BSA alerts and documenting decisions.” You’ll be surprised how clarifying this exercise is.

Categorize. Which of those activities require judgment, relationships, or creativity? Which are information processing: data retrieval, synthesis, pattern matching, structured output? When you free your people from assembly work, they can focus on the high-value activities that drew them to banking in the first place.

Build the foundation. This is the work that matters most and gets talked about least. Refine your data. Contextualize it. Encode your business logic. Build the data infrastructure that turns your raw institutional knowledge into something an AI can reason with. This is a strategic investment, and it’s the step that separates institutions using AI from institutions talking about AI.

Deploy with precision. Start with one AI agent — conversational, accessible, embedded in your workflow — that takes on one specific, high-leverage activity. Credit memo drafting. Loan covenant monitoring. Exception tracking. Whatever generates the most time savings for the most people. Prove the value, build trust, then expand.

The Efficiency Ratio Is a Lagging Indicator of a Leading Decision

Every CEO I talk to cares about their efficiency ratio. It’s one of the clearest measures of how well an institution converts revenue into profit. But here’s what I’d encourage every leader reading this to consider: the efficiency ratio of the future won’t be driven by the same levers as the efficiency ratio of the past.

It will be driven by how effectively your people are equipped to do their work. It will be driven by whether your institution has built the data infrastructure to let AI do what AI is uniquely qualified to do, so your people can do what they’re uniquely qualified to do. The institutions that invest in foundational, context-rich data work now will operate at a level of efficiency that sets them apart.

That’s the future driver of efficiency ratio. It’s not a dashboard. It’s not a chatbot bolted onto your website. It’s a data foundation that knows your bank as well as your best banker does, and an AI layer that puts that knowledge to work, every day, at scale.

The opportunity is here. The path is clear. And the institutions that move now will be the ones that define what community banking looks like for the next generation.

Turning Missed Moments into Meaningful Connections

Turning Missed Moments into Meaningful Connections

How AI Drives Deposit Growth by Amplifying the Human Touch in Community Banking

Related Content

Nothing found.

Digital Transformation in Community Banking Webinar

Digital Transformation in Community Banking

With the help of AI technologies, community banks have successfully been able to strengthen relationships, reduce churn, increase deposits, and improve ROI enterprise-wide by utilizing the data they already have at their fingertips—and your organization can, too. However, successful digital transformation can be a major challenge for midsized and community-based banks. Adopting new technologies, shifting operational mindsets, and hiring the talent necessary to build and execute upon AI solutions is a major endeavor. Many banks do not even know where to begin. In this presentation, discuss the steps and considerations for aggregating data across your bank to create a 360-degree view of your customers, why that is important, and ways other community banks have found success through analytics initiatives.

Related Content

Nothing found.

Staying Secure: Recent Security Breaches and Essential Prevention Strategies

The increasing reliance on digital technologies has led to the increased frequency of security breaches. Recent incidents have highlighted vulnerabilities across several industries, emphasizing the importance of robust cybersecurity measures. Here, we examine some notable security breaches that have recently made headlines, detailing the “how” and the responses taken to mitigate future risks.

Microsoft Azure and Executive Accounts

In a significant cyberattack on Microsoft Azure in January 2024, hackers exposed the accounts of hundreds of Microsoft senior executives to unauthorized access, with the use of phishing attacks and malicious links. The attackers used a password spray attack to break into the accounts, which is when an attacker tries several passwords across multiple user accounts to avoid detection systems. This breach allowed unauthorized access to Microsoft email accounts, leading to the exfiltration of sensitive emails and attached documents. The attackers also targeted source code and infrastructure, emphasizing the importance of heightened vigilance against sophisticated phishing tactics.

One extremely effective way to ward against this type of attack is to create strong passwords and change them regularly to prevent them from being hacked, as well as using multi-factor authentication.

Bank of America Third-Party Data Breach

Attackers understand that large banks have robust cybersecurity measures to protect their networks. However, many third parties lack similar resources and may not yet prioritize cybersecurity education or infrastructure. This makes them more likely to be targets for cybercriminals seeking vulnerabilities to exploit when sharing data with major institutions. This incident underscores the critical need for financial institutions to strengthen third-party vendor security protocols and ensure robust data protection measures.

The ransomware group LockBit orchestrated a breach targeting Bank of America in February 2024 via its third-party vendor, Infosys McCamish. Personal information—including names, Social Security numbers, and account details of over 57,000 individuals—was compromised.

Ascension Ransomware Attack

Such attacks necessitate comprehensive cybersecurity strategies to safeguard critical healthcare infrastructure and ensure uninterrupted patient care. Moreover, ensuring robust disaster recovery plans and reliable backups can get services back on track faster, which is particularly crucial for healthcare systems, because extended delay can directly impact patient care and safety.

Ascension, the owner of 15 hospitals in Michigan, fell victim to a ransomware attack in May 2024 that disrupted electronic health records systems, phone systems, and scheduling processes. Non-emergency procedures and appointments were suspended, highlighting the operational impact of cybersecurity incidents on healthcare services.

New York City Metropolitan Transportation Authority (MTA) Cyberattack

In 2020, research showed that municipalities, which are already vulnerable targets for cybercrime, faced 44% of global ransomware attacks—equating to approximately 133,496,000 incidents. An April 2021 cyberattack on the New York City Metropolitan Transportation Authority (MTA) compromised 18 systems, including those controlling train operations and safety mechanisms. This breach posed serious implications for public safety and operational continuity.

Following the attack, MTA swiftly implemented federally recommended security enhancements and mandated password changes and VPN switches for employees and contractors, illustrating proactive steps to fortify cybersecurity defenses.

Moving Forward: Prevention Procedures

Preventing security breaches requires a multi-faceted approach that empowers teams and safeguards organizational assets. Regular training sessions are essential to educate employees on identifying phishing emails, creating robust passwords, and understanding the importance of safeguarding sensitive information. This measure ensures everyone understands their role in preventing data breaches.

Strengthening asset management through classification, organization, automation, and continuous monitoring helps maintain an up-to-date inventory, facilitating informed decision-making and enhancing troubleshooting capabilities. Effective management and monitoring of access rights, supported by IAM, routine account audits, SSO, and multi-factor authentication, are also critical for ensuring only authorized personnel have access to certain resources.

Another strategy to prevent security breaches is implementing robust firewalls and antivirus software services, which can serve as the frontline defense against malicious threats. Regular updates to these defenses are crucial to identifying and addressing vulnerabilities promptly. Additionally, implementing automated data backup systems across multiple locations provides a safety net against data loss and physical damage, ensuring business continuity even in the face of unforeseen incidents. By integrating these preventive measures into comprehensive cybersecurity strategies, organizations can effectively mitigate risks and protect sensitive information from increasingly sophisticated cyber threats.

At Aunalytics, we are committed to preventing security breaches—protecting customer data is our top priority. We adhere to stringent security protocols, including regular employee training, robust encryption measures, and continuous monitoring of access controls. Our goal is to ensure our clients are utilizing the latest security technologies and best practices to stay protected, while having the right backup and disaster recovery strategies in place to get their businesses back up and running as quickly as possible in the event of a cyber event or disaster scenario.

Banking Forward: Analytics Trends in Financial Services

Banking Forward:

Analytics Trends in Financial Services

In the world of financial services, staying ahead of competition means embracing analytics trends that enhance customer and member experiences and operational efficiency. As technology continues to reshape the industry, financial institutions are turning to advanced analytics solutions to gain insights on customer and member behaviors.

Higher Customer and Member Engagement through Online and Mobile Services

Improving the online and mobile experiences is at the forefront of modern banking strategies. Institutions are not only investing in robust mobile banking apps but also leveraging app data to gain deep insights into customer or member behavior. By analyzing transaction patterns, engagement metrics, and user feedback, banks can uncover valuable insights that inform strategic decisions and improve service offerings. This increased access to mobile services significantly enhances the customer and member experience by providing convenient access to financial information anytime, anywhere.

It’s important to note that improved mobile services play a crucial role in shaping personalized experiences, which have become a cornerstone of customer engagement in the banking industry. Through advanced analytics, banks can decipher intricate client data to understand their preferences, goals, and financial behaviors. This allows them to create tailored advice and personalized financial plans on a large scale. Detailed client profiles allow banks to anticipate needs and offer relevant products and services proactively, thereby enhancing customer satisfaction and loyalty.

Highly Personalized Advising

Advising Services, like personalized experiences, is another solution that ensures each client receives tailored assistance aligned with their specific needs. Advising Services have evolved significantly with the integration of customer relationship management (CRM) technology. By using CRM tools, banks can compile comprehensive customer profiles enriched with transaction history, communication preferences, and financial goals. This wealth of data allows financial advisors to deliver customized guidance that addresses each customer’s unique circumstances and aspirations. Such personalized advisory services foster stronger client relationships, driving loyalty and retention in a competitive market.

Enhanced Customer Service through AI-Powered Chatbots

Similarly, AI (Artificial Intelligence) is revolutionizing customer interactions within the banking sector and how they might seek out help. AI-powered chatbots are being deployed to handle routine inquiries and provide instant assistance, reducing wait times and enhancing customer satisfaction. These chatbots are integrated seamlessly into banking platforms, offering users real-time support and guidance. Moreover, AI-driven virtual assistants are being used to deliver personalized money management tips, empowering customers and members with actionable insights to make informed financial decisions.

Open Banking Initiatives

And while AI is implemented to assist clients, open banking ensures that clients retain ultimate control over their data. Open Banking represents a new era of connectivity and collaboration in financial services. By securely sharing customer information through APIs (Application Programming Interfaces), banks can build partnerships with third-party applications and services. This integration allows for enhanced functionalities such as aggregated financial insights, streamlined payment processes, and personalized financial recommendations.

Predicting and Preventing Fraud and Cyberthreats

Finally, with the increase of cyberthreats and ransomware, cybersecurity and fraud detection continue to trend as well. Effectively identifying and mitigating malicious threats calls for strategic planning and investments in tools and infrastructure. Investing in cybersecurity further enhances customer and stakeholder trust by committing to protecting their data and assets.

In conclusion, the banking and credit union sectors are embracing advanced analytics trends to enhance customer experiences, streamline operations, and drive sustainable growth. By leveraging technologies like AI, CRM, and open banking principles, institutions can deliver personalized services that cater to individual needs and preferences effectively. Embracing these trends not only positions banks as industry leaders but also ensures they remain relevant and responsive to evolving customer expectations in a digitally-driven world.

At Aunalytics, we are committed to empowering community banks and credit unions with cutting-edge solutions that leverage these trends. By partnering with us, community banks and credit unions can optimize their operations, strengthen customer and member relationships, and prevent cyberattacks and fraud events that can erode consumer trust. We believe in supporting our clients to ensure that they remain at the forefront of the financial services sector.

Becoming More Customer-Centric—How Community Banks and Credit Unions Can Cultivate This Mindset and Act on It

Personal, white glove service has always been a competitive advantage for community banks and credit unions. Therefore, a customer-centric mindset is vital. While a customer may be just another number at a large, national bank, community-based financial organizations can get to know people on a more personal level—and they may in turn feel a larger sense of connection and loyalty to a bank or credit union that has a history within the community.

But, as banking moves to be more digitally-focused, a familiar, friendly face at the bank counter is not enough, especially as younger generations embrace the convenience of online and mobile banking. Customer touch points are increasingly digital—which isn’t necessarily a bad thing. Financial institutions now have a wealth of data about each individual. Large, national banks are already using this to their advantage.

Many large financial institutions have invested billions in technology, including data and AI-based solutions that allow them to fully embrace customer centricity in their business practice. This allows them to foster relationships based heavily on digital interactions.

But without ample resources that can be focused on developing data-backed solutions, how can a smaller, community-based institution compete?

Adopting a Customer-First Mindset

While a focus on the customer or member is the bread and butter of most community banks and credit unions, there is always room for improvement. While customer centricity is a sought after ideal, only about 9% of organizations have achieved this goal. This can make it a competitive differentiator for organizations who manage to fully embrace this mindset. To become a truly customer-centric organization, it’s not enough to provide a high level of customer service. It requires customer centricity to be embedded in the organization’s DNA and across all functional areas of the financial institution.

A customer’s interaction with an organization goes beyond the tellers at the branch, or a mobile app’s user interface (though these are each vitally important elements!) There are some questions to consider when evaluating whether an organization is truly putting the customer first:

- Are your products and services what your customers really want and need?

- Are recommendations and advice being tailored to each unique individual?

- Are customers experiencing seamless interactions across all touchpoints?

- Are you using direct feedback and data to inform decision-making?

- Are you able to provide customers with “unexpected value,” beyond what they would normally expect from their financial institution?

In order to reach these lofty goals, organizations must first get buy-in across the organization and actively work to shift goals and mindsets.

Embracing The Power of Data and AI

Once a bank or credit union has determined that it is on its way to cultivating a customer-centric mindset, it is time to start taking action. One of the most powerful ways to become more customer-centric is to rely on insights from data. But the first step is to organize data into a 360-degree view of each customer—breaking down data silos in order to capture the entire customer journey.

Once data has been aggregated, cleansed, and organized around each customer, it can be used to make data-driven decisions, personalize the customer journey, and increase the effectiveness of marketing campaigns, and optimize operations. With the power of AI and predictive analytics, organizations can:

- Enhance digital interactions with chatbots;

- Enact offer relevant product suggestions;

- Determine which customers or members are most likely to churn;

- Identify potential new customers who look the most like their current best customers;

- Optimize loyalty programs to increase customer satisfaction; and more.

Where To Start?

If all of this sounds like a lofty goal, that is because it is. This undertaking can be a huge challenge for most midsized banks and credit unions. In many cases, it could take several months—or even years—to get to this point. That is why many organizations are looking outside their own walls to work with experienced partners to guide them through the process along with pre-built technology solutions that can reduce the time to implementation.

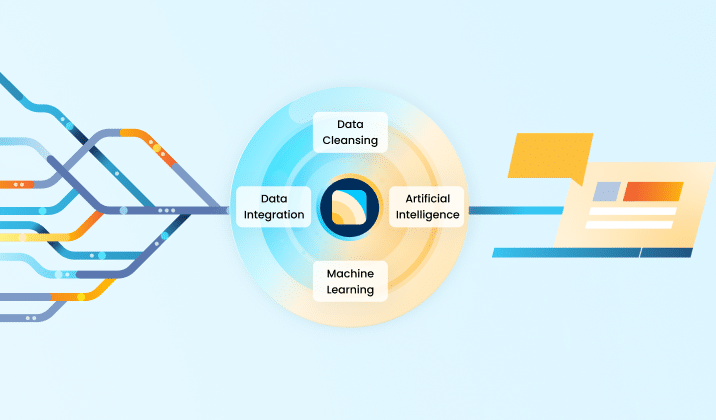

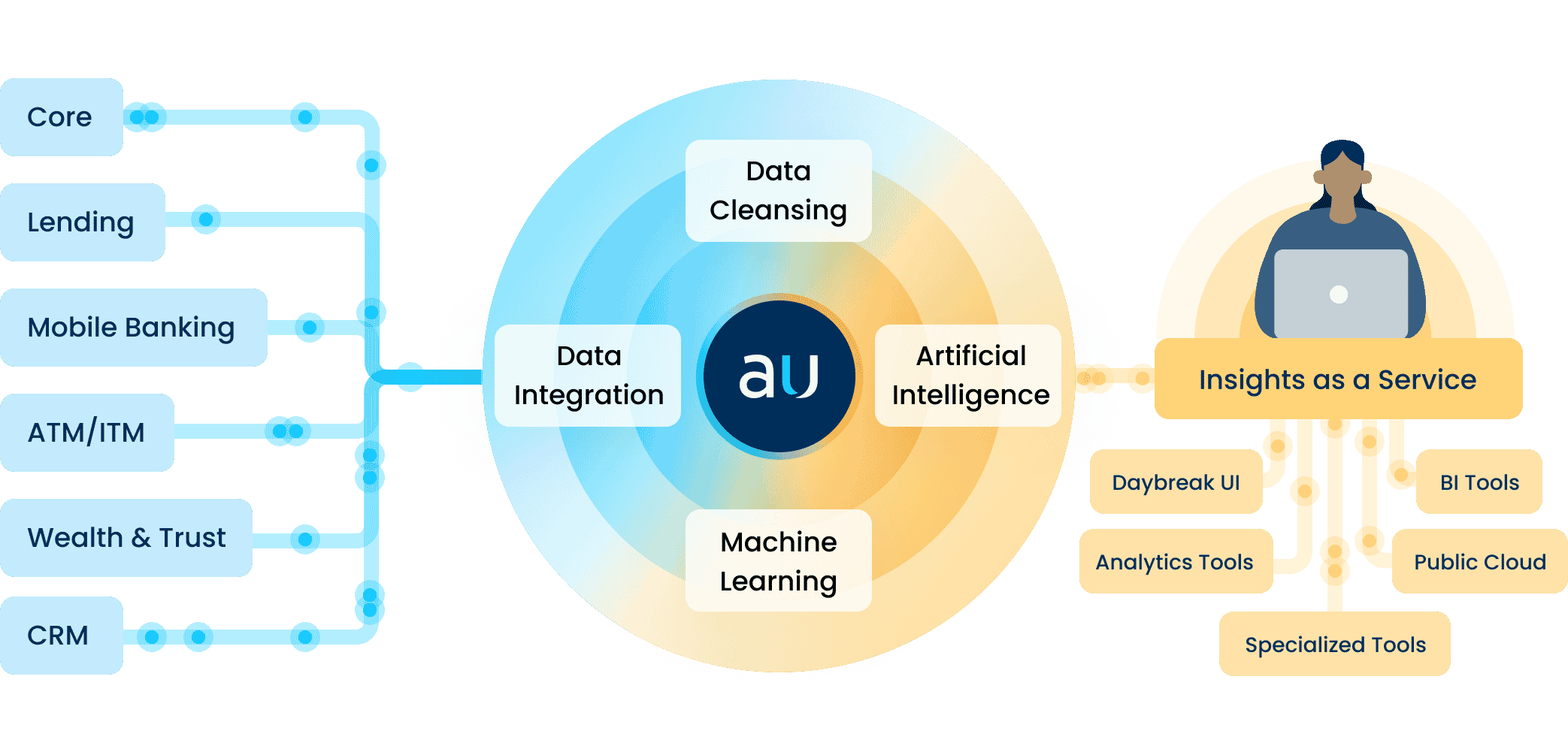

To meet the unique challenges of community banks and credit unions, Aunalytics has developed the Daybreak Analytics Database—an end-to-end data and analytics platform using AI and machine learning to enrich a bank or credit union’s existing data and create a customer-centric view. This ultimately allows midsized financial institutions to more effectively identify and deliver new services and solutions so they can increase wallet share and better compete with large financial institutions.

Financial Institution Cyber Attacks Are on the Rise—Your Institution Is Not Immune

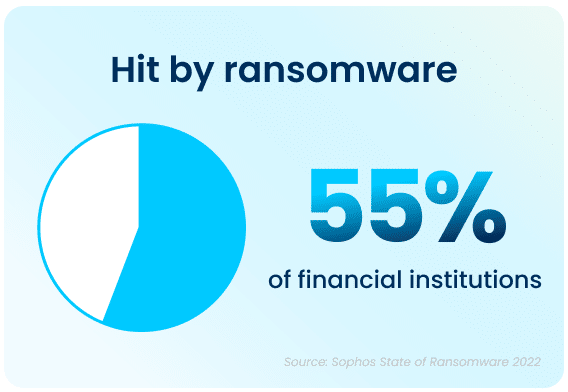

With recent uncertainty in the economy and bank closures hitting the news this year, you may be scrambling to find ways to increase deposits to protect your institution. But a larger, more urgent risk has always been lurking. With over half of financial institutions reporting cyber attacks in a single year, your organization may be next.

Nearly every day we learn of new horror stories from financial institutions who were the victims of elaborate attacks—in fact, 55% reported being a victim of a cyber-attack in a single year.

Bad actors are becoming more sophisticated in their methods. These prevalent attacks have high costs to your business uptime and productivity. A bad attack can also damage your reputation due to closure and data loss, while still costing your bank or credit union large sums of money to pay off ransoms—and you may not even get all of your data back.

Financial institutions hit by cyber-attacks pay, on average, $272,655 in ransom payments. And the average overall cost to remediate the ransomware attack in this sector is $1.59 million.

Do you know where your data lives?

Where you store your data matters, and your storage location may not be optimal for disaster recovery. Storing your backups locally, even if located at another of your facilities, may not protect your data from unknown risks.

In-house servers require large capital expenditures, and you miss out on economies of scale for regular upkeep and maintenance. Giant vendors may seem convenient, but you won’t know exactly where your data resides, and you lose control over the environment.

There’s a better way—Aunalytics backup and disaster recovery solutions can help you avoid losing data or paying large ransoms. We offer concierge solutions tailored to community banks and credit unions—helping you stay steps ahead of increasingly malicious attackers.

Backup and disaster recovery solutions enable the continuous operations of an organization during a disaster event, whether it involves a set of networks or servers, or when all primary IT services have become unavailable. Our solutions leverage the power of data, analytics, and Machine Learning. Disaster Recovery Services, coupled with a comprehensive backup and archival strategy, allow you to remain confident that you are prepared should your business encounter a disaster event.

Investment in Artificial Intelligence is Vital for Banks and Credit Unions

Has your bank or credit union made investments in artificial intelligence yet?

Advances in artificial intelligence (AI), and the promise it holds for the future, have been making news all year. And it’s no wonder that financial institutions are taking notice—a recent survey from the Economist Intelligence Unit found that 77% of bankers believe that unlocking value from AI will be the differentiator between winning and losing banks. Yet, many institutions are falling behind in AI maturity.

Despite its promise, making a large investment in artificial intelligence may seem risky to many midsized financial institutions. Hiring talent, developing a data management and analytics strategy, building a data platform, and creating AI models can be both time- and resource-intensive. Banks and credit unions want to ensure that the efforts spent to get an AI program off the ground will yield a high ROI, especially in times of economic uncertainty. Yet, failure to innovate and make progress toward digital transformation is not always an option in the highly competitive landscape.

Financial institutions find many uses for AI technologies

Thankfully, an investment in artificial intelligence can improve many processes across an institution. AI can optimize both time- and resource-intensive tasks, decrease risk, and increase revenue by improving the customer experience. For instance, by applying AI and machine learning algorithms to transactional data, banks and credit unions can gain insights into customers or members’ habits and preferences. Some use cases include:

- Detecting and preventing fraud

- Identifying loan default risk at the time of application

- Predicting customer churn

- Winning back business by discovering customer payments going to competitors, and subsequently making a more attractive offer

- Predicting the next best product for each customer then targeting them with the right product at the right time

- Calculating customer value scores in order to better allocate resources to target more valuable customers

Don’t get left behind

Large banks are already utilizing artificial intelligence use cases at scale. In a recent letter to shareholders, Jamie Dimon, Chief Executive Officer of JPMorgan Chase wrote, “Artificial intelligence (AI) is an extraordinary and groundbreaking technology. AI and the raw material that feeds it, data, will be critical to our company’s future success—the importance of implementing new technologies simply cannot be overstated.”

Because of this focus, his company has made tremendous investments in AI. They currently have over 300 AI use cases in production, and employ almost 3,000 people in data management, data science, and AI-research-related roles. This underscores how vital these new technologies are to success in the future.

Unfortunately, not every institution has access to talent and technology at the scale of JPMorgan Chase. That’s why Aunaytics has developed a cloud-based data and analytics platform to provide data management, advanced reporting, and predictive AI and machine learning solutions for midsized community banks and credit unions.

Daybreak for Financial Services allows institutions to learn more about their customers and members in order to provide a better overall experience—which in turn reduces risk, increases wallet share, and reduces expenses.

Why You Should Include an Analytics Platform in your Banking Software Arsenal

Banking software is vital to the success of all financial institutions. With an increasing focus on digital transformation, banks and credit unions amass a collection of platforms and software systems. Financial institutions not only rely on their banking core, but also CRM systems, online and mobile banking applications, loan management software, payment processing systems, and wealth management, risk, and compliance software, to name a few. Not only do these systems make banking more efficient, but they are collecting data that can be used to improve the business itself.

How can financial institutions best utilize their existing data? Thanks to their existing banking software, every institution holds valuable information about each customer or member that can be used to increase their lifetime value. PWC estimates that banks can generate a 70% return on initiatives targeting existing customers versus 10% when targeting new customers. Therefore, one of the best ways to use data to achieve better returns and higher margins is to focus on improving the customer or member experience.

Having access to an abundance of data points across various systems presents a tremendous opportunity to strengthen existing relationships—but it also poses a challenge. While each banking software system includes valuable information, it does not give the whole story. The problem for many institutions is that they have no way of getting a complete, 360-degree view of each individual from disparate software systems.

The Importance of an Analytics Platform

That is why a data and analytics platform is essential. An analytics platform can aggregate data from multiple systems, cleanse and organize that data into a 360-degree customer view, then apply artificial intelligence (AI) and machine learning algorithms to gain data-driven insights.

Once an analytics platform has been implemented, there are many customer intelligence use cases that can help banks and credit unions target the right customers, with the right offer, at the right time, including:

- Gaining transaction insights – Gaining access to transaction data, paired with AI and machine learning, gives great insights into consumer spending habits and preferences.

- Identifying competitor payments – By mining transactional data, financial institutions can discover customer payments going to competitors, then use that information to reach out to customers or members and win back business with a more attractive offer.

- Generating product recommendations – With access to data points from several software systems, machine learning and AI models can make predictions such as the next best product to offer for each customer.

- Predicting churn – AI algorithms identify trends in transactional data, and determine which customers are most likely to churn—so financial institutions can take actions to prevent it.

- Calculating Customer Lifetime Value – An analytics platform can calculate customer value scores based on a large number of relevant data points using AI and machine learning. Banks and credit unions can use this information to allocate resources toward targeting customers with higher customer lifetime value scores.

These are just a few of the ways banks and credit unions can implement insights from a data and analytics platform that mines data from across their organization’s many software systems. Once the platform is implemented, any number of use cases can be developed using AI and machine learning—getting the data collected, aggregated, updated, cleansed, and organized for analytics is one of the largest obstacles for organizations.

Thankfully, Aunalytics has developed a robust data and analytics platform called Daybreak for Financial Services. Daybreak provides all of these services and more to make sure your bank or credit union is making the most of its banking software data to reduce risk, optimize processes, increase revenue, and most importantly, improve the customer or member experience.

The Truth About Artificial Intelligence in Business

Is the existence of Skynet imminent or is that simply a sci-fi trope? In this brief video, Dr. David Cieslak, Chief Data Scientist at Aunalytics, talks about the capabilities of Artificial Intelligence in business, some potential concerns with AI, and where the technology is headed in the future.

While there exists a broad range of applications for AI, in the business world, this technology has the potential to drastically change how we understand our customers and how we use our data to interact with them. Once created and trained with customer data, AI has the ability to quickly provide suggestions and insights that would otherwise be prohibitively difficult or even impossible to observe on your own.

For example, Aunalytics’ Daybreak for Financial Institutions platform uses a proprietary AI model that can predict when a customer or member is likely to churn, to suggest which product to promote based on what that specific person is most likely to buy, to identify where the best branch locations are, and more. These types of insights are hiding in your data, simply waiting to be uncovered. To learn more about the business applications of AI, you can view the extended interview here.

David Cieslak, PhD, is the Chief Data Scientist at Aunalytics since its inception and leads its Innovation Lab in the development and delivery of complex algorithms designed to solve business problems in the manufacturing/supply chain, financial, healthcare, and media sectors. Prior to Aunalytics, Cieslak was on staff at the University of Notre Dame as part of the research faculty where he contributed on high value grants with both the federal government and Fortune 500 companies. He has published numerous articles in highly regarded journals, conferences, and workshops on the topics of Machine Learning, Data Mining, Knowledge Discovery, Artificial Intelligence, and Grid Computing.