Turning Missed Moments into Meaningful Connections in Community Banking

Article

Turning Missed Moments into Meaningful Connections:

How AI Drives Deposit Growth by Amplifying the Human Touch in Community Banking

Community banks and credit unions have always had a competitive edge: deep, trusted relationships with their customers and members. But in today’s environment, where digital expectations meet lean staffing and fragmented systems, even these institutions face a new kind of challenge.

Large banks are investing billions in AI to replicate what community banks do naturally — build relationships. According to Citibank, 93% of financial institutions expect AI to improve profits within five years, potentially unlocking $170 billion in industry-wide gains by 2028.

Yet the real issue facing community-based financial institutions isn’t just technology. It’s a quiet acceptance of the limits of human capacity — and the tolerance of inefficiency.

The Core Challenge: Banking Has Normalized Missed Opportunities

Most community financial institutions today have accepted that front-line staff can only do so much. Customer-facing personnel like branch managers, private bankers, and relationship bankers are responsible for hundreds, sometimes thousands, of customer relationships. With each client holding multiple accounts and generating thousands of transactions, it’s become operationally impossible to deliver the kind of proactive, personalized service that defines the brand of community banking. Without the tools to monitor every customer’s needs in a timely manner, they’re often limited to engaging only with the individuals who walk into the branch or proactively reach out to the bank or credit union.

The Result: A Culture of Firefighting

A customer quietly transfers funds to a competitor — and no one follows up.

A member switches jobs, prompting financial changes that go unnoticed due

to a lack of timely alerts.

A well-connected team member at a large local employer with referral potential is never identified as an influencer.

These moments aren’t missed due to lack of care or intention. They’re missed because banks and credit unions have had to accept the limits of their current staffing models and tools. Hiring enough employees to cover every opportunity would be cost-prohibitive. So, institutions settle for staffing formulas that prioritize coverage

over connection.

But what if you didn’t have to choose?

The Opportunity: Use AI to Scale Personal Service Without Scaling Headcount

That’s where Aunalytics comes in. Their solutions enable front-line staff to engage with all of their customers — not just those who raise their hands — by surfacing key activity signals and recommending the right time and message to connect. It empowers every banker to be in the right place, at the right time, which ultimately can lead to a net increase in core deposits. Rather than accepting that proactive service is too expensive, Aunalytics uses AI to unlock it at scale. It analyzes transactional and CRM data to uncover key relationship signals and delivers them directly to the banker or credit union professional. No combing through dashboards. No digging. Just timely, actionable insights tailored to each role.

Now, community-based financial institutions can identify critical relationship moments before they’re lost — retaining deposits, strengthening loyalty, and generating new business without increasing headcount.

Furthermore, Aunalytics goes beyond delivering a software solution by offering a strategic partnership that includes hands-on guidance and deep industry expertise. Every engagement includes a dedicated team of data engineers and analytics experts who guide implementation and support long-term success. This hands-on approach ensures institutions are not left to interpret or operationalize AI insights on their own.

The Critical First Step: An Intelligent Data Warehouse

The most important component of all AI systems is the quality and structure of the data itself, and the data model referenced to generate answers and perform humanlike tasks. Without a solid data foundation, AI efforts often struggle with fragmented, inconsistent, or incomplete data, limiting their effectiveness and scalability. Therefore, the first step is to create a reliable knowledge base to serve as the source of truth. In order to facilitate impeccable accuracy and traceability, Aunalytics has developed an Intelligent Data Warehouse and data model specific to community-based financial institutions to set their data and analytics initiatives up for success.

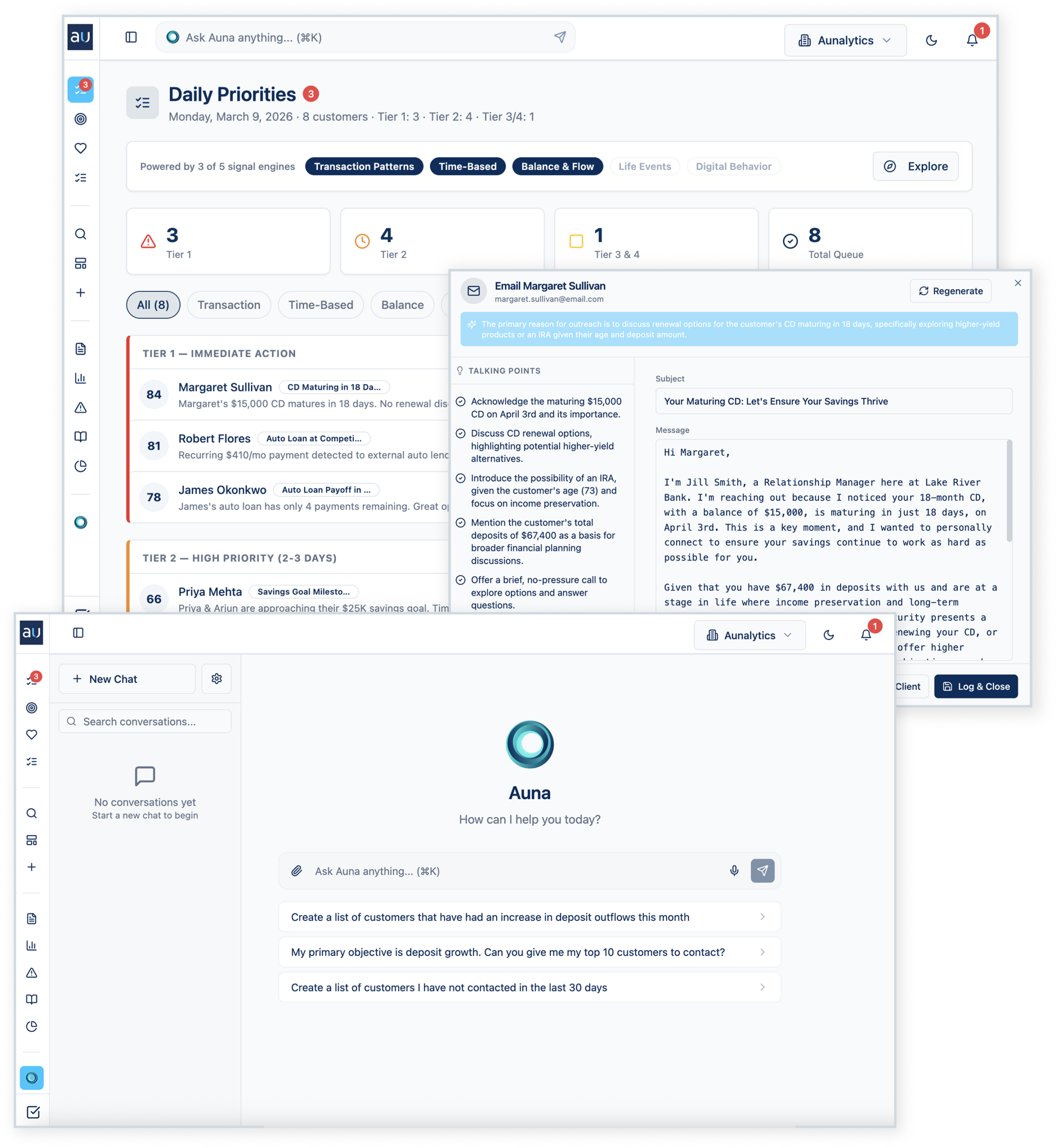

Auna: Insights That Find You

Auna is designed to help mid-sized financial institutions do work that drives growth. This approach shifts institutions from reactive responders into proactive relationship-builders, without requiring more people or more hours. Some of its main components are:

Daily Priorities: Instead of relationship managers pulling reports or digging through their email, Auna scans thousands of transactions from the last 24 hours, cross-references them against months of trend data, runs them against your institution’s playbook, and surfaces the five things you need to do today.

Personalized Outreach: Auna not only surfaces who should be contacted and when, but it takes it a step further and generates a personalized outreach message on the spot.

Conversational Chat: A private, natural language interface that allows any staff member to query near real-time data — no technical expertise required.

Examples in Action

- Retention: A high-value client moves a large sum to a competitor. Auna detects the transaction and prompts immediate outreach.

- Engagement: A shift in direct deposits signals a life transition. Staff receive an alert to check in and support the customer.

- Acquisition: A potential advocate is identified based on network or employer data, prompting the launch of a referral playbook.

Designed for Action, Not Analysis

Traditional BI tools often lead to “dashboard fatigue,” where the sheer abundance of data fails to drive business outcomes and the analytics are underused or overlooked. Auna elevates the focus from analysis to action. By surfacing just the insights that matter, right when they matter, bankers can spend precious time on relationships, not reporting. Even a few hours saved per week per employee compounds into hundreds of hours redirected to higher value activity across the institution.

Unlike dashboards that sit unused, Auna’s notifications are consistently read and acted upon. And the natural language chat feature ensures no question is too complex or too technical to answer.

A Modern Strategy for a Human-Centered Mission

Community financial institutions shouldn’t be forced to choose between digital efficiency and human connection. With Auna, they can have both. AI becomes an extension of their relationship model — empowering staff to drive growth by acting on what matters, when it matters, at a scale previously impossible. Because in a world of automation, relationships still win — and now, they can win at scale.

The Efficiency Ratio Problem No One Is Actually Solving

Article

The Efficiency Ratio Problem No One Is Actually Solving

Every year, we attend banking conferences and hear advice echoed from stage after stage: “Get your data together to use AI.” It’s become a mantra in the industry. Everyone agrees it’s important, and then most go home and nothing meaningfully changes.

Data matters. And the leaders I talk to know it matters. The part that many miss today is understanding what “getting your data together” really means. That gap, between the slogan and the substance, is good news. It means the biggest opportunity to improve your efficiency ratio is still in front of you.

The Advice Everyone Gives but Nobody Finishes

When most people talk about getting your data together, they mean integration. Pull it from your core, your loan origination system, your CRM, your general ledger, and get it into one place, maybe a dashboard. Consolidated reporting is better than fragmented reporting, but if the end goal is using artificial intelligence to drive your efficiency ratio, then integration is step two of a ten-step journey.

The good news? The next steps are clearer than you might think.

What “getting your data together” really means is something far more granular and far more valuable. It means refining your data. It means embedding business context, encoding the business logic of your specific bank. It means having your data ready to use AI. Once you understand that distinction, the path forward becomes surprisingly actionable.

What Is a Data Foundation, Really?

A properly built data foundation is the unlock to using AI. It’s the key to doing the work you already do, but quicker, easier, and smarter.

Context matters because an LLM is extraordinary at processing language, identifying patterns, and generating output. What it cannot do, on its own, is understand that when your bank says, “Primary Relationship” or “Class 3 commercial real estate,” it means something slightly different than when the institution next door says the same thing. It doesn’t know your policy exceptions, committee preferences, or the dozen small decisions your best banker makes without even thinking about them.

That’s business logic. And every bank’s logic is different, which is a strength. Your institutional knowledge is a competitive asset. The data foundation doesn’t just store your data. It teaches AI how your bank actually works, preserving and scaling the expertise your team has built over years.

The Credit Memo Example

Take credit memo writing. It’s the example that illustrates the opportunity clearly, and once you see it, the same pattern shows up across the institution.

A credit memo is a structured synthesis of financial data, borrower history, market context, policy compliance, and risk assessment. It’s organized in a way that tells a clear story to a credit committee. It requires knowledge, context, and consistency.

A commercial banker and credit analyst might spend hours on a single credit memo. Not because the intellectual work is that complex, but because the assembly is. Pulling data from multiple systems, cross-referencing financials, ensuring the narrative aligns with current policy, formatting it correctly, reviewing it for completeness. Your bankers shouldn’t be spending their best hours on assembly.

Now the exciting question: what is stopping AI from writing that credit memo?

Frontier LLMs can synthesize, analyze, and write at extraordinary levels. What’s stopping them is context and business logic. The AI doesn’t know your bank’s specific credit policy. It doesn’t know how your committee likes to see deals presented. It doesn’t know that your chief credit officer always wants to see the debt service coverage calculated a certain way, or that your institution has a specific appetite for owner-occupied CRE that differs from the industry norm.

But if you’ve built the data foundation, if you’ve done the important work of refining your data, embedding your context, and encoding your logic, then an AI agent can draft that memo in your format, with your logic. The commercial banker reviews it, applies judgment, and moves on to the next relationship. The work that took hours now takes minutes. Multiply that across your team, across your branches, across a year, and you’re looking at a meaningful shift in your efficiency ratio from a single AI capability: writing credit memos.

A Framework for Doing This

So what does this look like in practice? I’d suggest a framework that starts with the work, rather than the tech.

Decompose. Pick a role: commercial banker, credit analyst, branch manager, compliance officer. Map the activities that role performs. Be specific. Instead of “lending,” think “spreading financials from tax returns.” Instead of “compliance,” think “reviewing BSA alerts and documenting decisions.” You’ll be surprised how clarifying this exercise is.

Categorize. Which of those activities require judgment, relationships, or creativity? Which are information processing: data retrieval, synthesis, pattern matching, structured output? When you free your people from assembly work, they can focus on the high-value activities that drew them to banking in the first place.

Build the foundation. This is the work that matters most and gets talked about least. Refine your data. Contextualize it. Encode your business logic. Build the data infrastructure that turns your raw institutional knowledge into something an AI can reason with. This is a strategic investment, and it’s the step that separates institutions using AI from institutions talking about AI.

Deploy with precision. Start with one AI agent — conversational, accessible, embedded in your workflow — that takes on one specific, high-leverage activity. Credit memo drafting. Loan covenant monitoring. Exception tracking. Whatever generates the most time savings for the most people. Prove the value, build trust, then expand.

The Efficiency Ratio Is a Lagging Indicator of a Leading Decision

Every CEO I talk to cares about their efficiency ratio. It’s one of the clearest measures of how well an institution converts revenue into profit. But here’s what I’d encourage every leader reading this to consider: the efficiency ratio of the future won’t be driven by the same levers as the efficiency ratio of the past.

It will be driven by how effectively your people are equipped to do their work. It will be driven by whether your institution has built the data infrastructure to let AI do what AI is uniquely qualified to do, so your people can do what they’re uniquely qualified to do. The institutions that invest in foundational, context-rich data work now will operate at a level of efficiency that sets them apart.

That’s the future driver of efficiency ratio. It’s not a dashboard. It’s not a chatbot bolted onto your website. It’s a data foundation that knows your bank as well as your best banker does, and an AI layer that puts that knowledge to work, every day, at scale.

The opportunity is here. The path is clear. And the institutions that move now will be the ones that define what community banking looks like for the next generation.