The AI Compute Constraint and the Case for an Intelligence Layer

Article

The AI Compute Constraint and the Case for an Intelligence Layer

On May 6, Anthropic announced a new compute partnership with SpaceX. Buried in the announcement was a number that should reframe how every CIO in a regulated industry plans their 2026 AI roadmap: Anthropic is projecting roughly 80x demand growth in Q1 2026.

If that number holds, the race has shifted to compute, infrastructure, and orchestration capacity. The winners will be the enterprises that build an Intelligence Layer: the discipline and architecture to know when not to use frontier models.

For the last couple of years, enterprise AI strategy has had a simple shape: pick a frontier model, point your workflows at it, and let intelligence flow. That worked when usage was experimental, costs were absorbed in innovation budgets, and compliance teams hadn’t yet asked the hard questions. It doesn’t work at the scale we’re now entering.

Three forces are converging on enterprise AI:

Frontier capacity is constrained, and the constraint is physical.

Anthropic's deals with SpaceX, Amazon, Google, Microsoft, and NVIDIA are a signal. The frontier labs themselves are telling us the binding constraint has moved from capability to capacity.

Frontier models are economically inappropriate for most enterprise tasks.

A regulated bank doesn't need a trillion-parameter reasoning model to classify a transaction or route a service ticket. Sending those tasks to a frontier endpoint is the equivalent of dispatching a corporate jet to pick up the mail. It works. But it also burns capital that should be funding actual differentiation.

Regulated industries can't tolerate opaque dependencies on a single model path.

When every workflow is wired directly to a frontier API, you inherit that vendor's outages, rate limits, data residency posture, and pricing changes, with no control plane to absorb the shock. For a CIO at a regulated institution, that arrangement belongs on a risk register, not an architecture diagram.

The architectural conclusion: an Intelligence Layer

The strategic message is clear: frontier intelligence is becoming too expensive and too scarce to sit in the direct execution path for every request. Enterprises that recognize this are moving toward an architecture where frontier models are a selectively-invoked resource rather than the default destination for every request.

We call this an Intelligence Layer, and it sits between your business systems and the model landscape. It does five things:

- Routes each request to the right tier of intelligence (frontier, specialized, classical ML, or a deterministic rule);

- Governs policy, data residency, masking, and audit at the routing point before any data leaves your environment;

- Contextualizes the right enterprise data into the right prompt without leaking the rest of the warehouse;

- Orchestrates multi-step agent workflows so a single business task doesn’t become a hundred opaque API calls; and

- Observes every decision, model call, cost, and latency, turning AI from a black-box expense into a measurable operational system.

Framed plainly, the Intelligence Layer is the economic control plane for enterprise AI. It’s what allows a CIO to answer the questions a board is starting to ask: What did AI cost us this quarter? Which workloads drove the cost? Which of those workloads needed a frontier model? Are we compliant? Are we resilient if our top vendor has an outage tomorrow?

The opportunity hiding inside the constraint

Here’s the part that gets missed in the headlines about GPU shortages and gigawatt deals: scarcity is clarifying. It forces enterprises to ask a question they should have been asking all along, “What is the right intelligence for this task?” instead of defaulting to the most intelligence for every task.

Banks that get this right will see lower AI run-rates, faster compliance reviews, and better outcomes from the workflows that genuinely need frontier reasoning, because those calls will no longer be competing with thousands of trivial requests for the same capacity.

IT leaders who get this right will have something they can defend in front of a board, a regulator, and an auditor: a documented, observable, governed system for deploying AI — not a collection of integrations stitched into production.

The compute race that Anthropic’s announcement signals is real, and it will reshape the economics of this industry. But for the CIO of a regulated enterprise, the strategic question is less about how much frontier capacity you can secure and more about how much of your business genuinely needs it, along with how disciplined you are about routing the rest.

That discipline is the moat, and the Intelligence Layer is how you build it.

Memory-Centric AI: Your Real Advantage Isn't the Model

Article

Memory-Centric AI: Your Real Advantage Isn't the Model

In April 2026, Andrej Karpathy published a short essay on Wikis for LLMs. His argument: the enterprises that win with AI will be the ones that build, govern, and refine the curated knowledge their AI systems draw on, not the ones with access to the best models.

For a CIO in a regulated industry, that argument lands differently than it does for a startup. The shift from model-centric to memory-centric AI is the most important reframing of enterprise AI in the past year, with direct implications for how you spend your 2026 AI budget.

The Shift from Model-Centric to Memory-Centric AI

For three years, enterprise AI strategy has been organized around models. Pick the best one, prompt it carefully, and upgrade when something better ships. Performance, in most board decks, is a function of model capability.

That framing is starting to break.

CIOs running these systems in production are finding that two enterprises using the same frontier model can produce wildly different AI outcomes. The variable is what the model has been told about the business: the policies, definitions, prior decisions, escalation paths, and institutional rules that turn a generic LLM into something that behaves like a useful colleague.

Karpathy gave that body of knowledge a name: a wiki for the LLM. We’ve been building it under a different name — resolutions — inside our IT operations agent for months. The terminology matters less than the architectural conclusion both arrive at: the durable AI advantage is the curated memory the system draws on, not the model it calls.

What This Looks Like in Practice

Consider a recurring problem in IT operations: a Windows build update fails on an end-user device. A model-centric approach treats every occurrence as a fresh prompt and the work product evaporates the moment the ticket closes. A memory-centric approach captures the resolution as a structured, durable artifact that records the context, troubleshooting steps, and escalation criteria. Every subsequent occurrence draws on it, so the model applies a vetted answer instead of re-deriving one.

The economic difference is significant. Inference costs drop because known problems stop consuming frontier compute, and resolution times drop because the system is executing rather than reasoning. For a regulated environment, the bigger payoff is auditability: you can point a regulator at the exact knowledge artifact that produced an outcome.

The Failure Mode No One Warns You About

There is a specific risk in memory-centric AI that we’ve watched play out in real systems, and it deserves a CIO’s attention before it shows up in your environment. We call it error baking.

When AI systems enrich tickets, documents, or workflows by drawing on prior outputs, any error embedded in those prior outputs gets reused, reinforced, and amplified. A resolution that was 80% correct becomes the source material for the next resolution, which is now 75% correct, which trains the next one, and so on. There is no single moment of failure, just a subtle compounding drift.

The fix is governance at the memory layer, not better models: a reviewed, version-controlled knowledge base the AI is allowed to draw on, kept separate from the raw outputs it generates. Without that separation, your AI gets worse over time, in ways that are nearly impossible to detect from outside the system. With it, the system improves with every resolved incident, because every resolved incident becomes a vetted asset the next one builds on.

For a CIO in a regulated industry, this is the difference between an AI investment that compounds and an AI investment that decays.

Owning The Memory Layer

The memory layer is not documentation, and it is not a side project. It is infrastructure. It belongs in the same conversation as your data warehouse, access controls, and audit logs — because functionally, it is all three.

Three questions a CIO should be asking now: Where does our AI’s institutional knowledge live today — in prompts, in chat histories, in individual employees’ heads, in scattered Confluence pages? Who owns the curation, review, and version control of that knowledge? Can we point an auditor at the specific artifact that produced a given AI output?

In financial services, healthcare, and government IT, the answer to that last question is going to determine which AI workloads are allowed in production at all.

The Reframe

The competitive advantage in enterprise AI will not belong to the organizations that access the most capable models. Those models are becoming a commodity, available to your competitors on the same terms they’re available to you.

The advantage will belong to the organizations that own — and govern — what their models know.

That asset compounds, a regulator can inspect it, and a competitor cannot replicate it by signing a different vendor contract.

The model is rented. The memory is yours.

Use AI to Determine, Not Just Infer: Why Declarative AI Matters

Article

Use AI to Determine, Not Just Infer: Why Declarative AI Matters for Regulated Institutions

AI companies are racing to convince you that their models are smart enough to figure out your business. However, most enterprise AI deployments quietly fail in the gap between that promise and what regulated institutions actually need — a gap that declarative AI is built to close.

You’ve probably sat through a compelling AI demo. Their model answers fluently, summarizes documents, and generates reports that look like what your team spends hours producing by hand.

But then someone in the room asks whether it knows how you define a primary banking relationship. They ask whether it applies your credit policy thresholds the same way every time, and what you’d show a regulator who questioned a decision it made. Those are the questions that separate AI that looks good from AI that works for your institution, in your regulatory environment, at the stakes you’re operating under.

The Flaw in Model-Centric AI

A growing number of AI vendors are building what are called model-centric systems, on the premise that a sufficiently capable model given enough of your data will figure out your business. The models are genuinely impressive, but model intelligence isn’t what solves the problem these institutions face.

Every regulated institution — community bank, credit union, company running enterprise IT under compliance requirements — operates on institutional knowledge that is declared rather than discovered. Your definition of a criticized asset, your risk rating thresholds, and your rules for what triggers a relationship review aren’t patterns hidden in your data waiting for a model to find them. They are decisions your institution has made, codified in policy, and required to be applied consistently across every loan review, compliance filing, and customer interaction.

When a model-centric AI system tries to apply your institutional logic, it doesn’t read your policy manual and execute it. It infers what your logic probably is, based on patterns in your data and whatever context you’ve fed it at the moment of the query. Every answer is a probabilistic approximation of a declarative truth.

That level of approximation is acceptable for marketing copy, but not for a credit decision, a regulatory disclosure, or a risk report going to your board.

Declarative AI vs. Inferential: The Distinction That Changes Everything

There are two fundamentally different ways to make an AI system work:

Inferential AI asks the model to reason its way to the right answer using whatever data and context you provide, making the model itself the intelligence layer. In theory, a better model produces better output. In practice, the model’s output varies based on how a question is phrased, what context was retrieved, and what version of the model is running, so there is no single authoritative answer, only the current best inference.

Declarative AI encodes your institutional logic into the data foundation before the model ever sees it, expressing your definitions, rules, and thresholds as an explicit, governed data architecture. The model doesn’t need to infer what “aggregate calendar-year deposits” means, because your intelligence layer has already defined and computed it. The job of the model is to reason over a foundation of established fact rather than construct that foundation on the fly.

For companies in regulated industries, it’s the difference between an AI system you can stand behind and one you can only hope doesn’t embarrass you in front of an examiner.

Why "Better Models" Aren’t the Solution

The standard vendor response is that models are getting better fast, and soon they’ll handle institutional complexity reliably. Models are improving rapidly, but improvement doesn’t resolve the declarative vs. inferential problem. A more capable model makes better guesses; it doesn’t turn guesses into facts. Your credit policy isn’t a pattern to be discovered at higher confidence levels. It’s a decision to be applied with complete consistency.

Governance is the dimension that will eventually land on a CEO or CIO’s desk personally. SR 11-7 and similar guidance require your AI systems to be explainable and auditable, which means when an examiner asks why a decision was made, “the model reasoned its way to this answer” isn’t a defense — it’s an admission. A governed rule with documented provenance is something you can put in front of a regulator, a board risk committee, or your own general counsel. Model weights are not.

There’s also a cost structure dimension that matters more the longer you run the system. Model-centric AI is a variable cost that scales with usage: every query, every user, every new workflow adds to the bill, and the more your institution embraces AI, the faster the number grows. Platform-centric AI is closer to a fixed cost you build once, where the marginal cost of additional use is near zero. Per-token prices will keep falling, but they won’t close this gap, because the volume of tokens required to re-derive your institutional context at query time doesn’t compress. By year three, the two architectures produce very different numbers on your P&L.

The Integration Problem Nobody Talks About

There’s a harder truth underneath all of this that the AI demos never address: most enterprise AI deployments fail not because the model isn’t good enough, but because the data isn’t ready.

Your customer records live in one system, transaction history lives in another, and loan origination data lives in a third. None of those systems were designed to talk to each other, and none of them have consistent definitions of shared concepts. “Customer” means something different in your core banking platform, your CRM, and your treasury management system.

Getting an AI model to reason accurately over that environment isn’t a prompt engineering challenge; it’s a data engineering one. It is the part most AI programs systematically underestimate. Resolving customer identity across a core banking platform, a CRM, and a treasury system, reconciling how Fiserv or Jack Henry structures accounts against your own definitions, and maintaining those definitions through core upgrades and acquisitions requires years of domain-specific work. When an AI initiative stalls or comes in over budget, this is almost always where it happened.

This is the work most AI vendors skip. They show you what the model can do once someone else has solved the data problem. They leave the data problem to you.

The data foundation is the moat — not because it’s expensive to build, but because it takes years to do right and it’s specific to your institution. When a competitor promises to replicate it with a smarter model, they’re proposing to shortcut a decade of domain-specific engineering. That’s not a technical claim. It’s a sales claim.

Three Things to Require Before You Commit Budget

If you’re a CEO or CIO evaluating AI investments, there are three things worth requiring of any vendor before you commit budget.

Require that your institutional logic lives in the data layer, not in the model or the prompt. Your definitions and business rules should be explicit, governed, and independent of the model, so they survive vendor changes, model upgrades, and staff turnover. If a vendor can’t show you where that logic lives, you’re being asked to store your institution’s intelligence inside someone else’s product.

Require a clear model-upgrade path that doesn’t put your institutional knowledge at risk. In a model-centric architecture, a model upgrade can invalidate the logic encoded in the current model, forcing you to revalidate your AI every time the vendor ships a release. In a platform-centric one, the intelligence layer is model-independent and the model is a swappable component. Ask your vendor to explain their upgrade path.

Require that every AI-supported decision be defensible to a regulator on its own terms. You should be able to point to the rule itself — when it was authored, what data it depends on, what it produces — not a description of what the AI probably did. If a vendor can’t produce that, you’re the one who will be asked to explain it.

Before deploying any AI agent or generative capability into a regulated workflow, verify that the underlying data is trustworthy, governed, and AI-ready, with resolved customer identity, codified business definitions, and derived intelligence maintained as standing metrics rather than computed on demand. Build incrementally, but anchor the roadmap on what architecture serves your institution in year three, not what you can show in thirty days. And insist on model independence, so that as foundation models improve, you benefit from the improvement without having to revalidate your institutional logic.

The AI companies competing for your budget are offering real capability, and the models are improving, but model capability is increasingly a commodity. What isn’t a commodity is a declarative AI foundation — governed, institution-specific, and built to give every model you deploy established fact to reason from. That foundation is what separates AI that works in a boardroom presentation from AI that works at 8 AM on a Monday, when your banker needs to know who to call, why it matters, and what to say — and needs to be sure it’s right.

AI is Only As Good As Your Data

Article

AI is Only As Good As Your Data

Every week, another AI vendor promises their platform will transform your financial institution. Better member insights, smarter lending decisions, and automated reporting. The pitch is compelling and the pressure to act is real.

Before you sign a contract, there’s a question worth asking: Do you actually have the data to back it up?

AI is only as good as the data underneath it. And most financial institutions don’t have the data that’s ready for AI yet.

The key is starting with your data foundation first.

For financial institutions, the challenge isn’t the amount of data, it’s the data readiness. When you skip the step of cleaning and structuring your data and go straight to the AI layer, here’s what happens:

- The AI produces answers that feel authoritative but are statistically probable, rather than being declaratively accurate.

- You can’t audit the decision: you don’t know why it said what it said.

- You keep running the same calculations over and over, driving up costs with every query.

This isn’t a tech failure. It’s a sequencing failure. The intelligence has to be built into the data before you hand it to an AI.

What "AI-Ready Data" Actually Means

AI-ready data has been transformed, enriched with business logic, and structured so that when a question is asked, the answer is calculated, not guessed.

Think of it this way: if you ask an AI to tell you which members are at risk of leaving this quarter, it needs more than raw transaction records. It needs a unified view of each member’s relationship with your institution, behavioral signals over time, and the business rules your team uses to define “at risk” in the first place. That context must be built in.

The intelligence is in the platform. You must build it into the data layer before AI can deliver answers you can trust and act on.

Two Approaches and Why They're Not Equal

Approach One: Ask the AI to Figure It Out

Some vendors take raw data, often pulled from a cloud warehouse, and let the AI model do the calculations on the fly. The model ingests your data, runs its analysis, and returns an answer.

This sounds efficient. It’s not. Every calculation runs repeatedly, consuming tokens and compute resources with each query. Costs scale with usage, not with value. And when you ask, “why did you flag this member?” the answer is a statistical distribution, not a reason.

Approach Two: Pre-Compute the Intelligence

The more effective approach, and the one Aunalytics is grounded in, is to do the hard work before the AI ever sees the question. Every relevant metric, every business rule, every behavioral signal is calculated, validated, and stored in a structured intelligence layer.

When a question comes in, the AI retrieves a precise answer from data that was already prepared for it. The result is faster, cheaper, more accurate, and fully auditable.

This is what we mean when we say Aunalytics makes data AI-ready.

What This Means for Your Institution

If you’re a CEO, CIO, or CTO at a financial institution, this distinction matters for three reasons:

- Accuracy: Declarative answers built on prepared data are more reliable than probabilistic outputs from raw data. When a banker acts on an insight, they need to trust it.

- Auditability: Regulators and examiners want to know why a decision was made. With pre-computed intelligence, you can show your work. With probabilistic AI, you can’t.

- Cost: Paying for compute on every query — at scale — adds up fast. Pre-computed data means you’re paying for results, not repeated calculations.

The Partner Question

Most community financial institutions don’t have the data science teams, the infrastructure, or the time to build this foundation themselves. They don’t need to.

But they do need a partner who’s already done the work — one who understands community banking deeply and can deliver production-ready AI data as a service.

That’s not a software tool. It’s not a dashboard. It’s a managed service built on years of experience working with the specific data structures, core systems, and regulatory environment of community banks and credit unions.

Aunalytics has been building and refining banking-specific data sets for over eight years. The Intelligent Data Warehouse isn’t a general-purpose platform adapted for banking. It was built for banking from the ground up.

Before you evaluate the next AI platform, ask the vendor one question:

What does your solution do to prepare my data for AI before the AI ever touches it?

The answer will tell you everything.

Start With the Right Foundation

The institutions that will win with AI aren’t the ones who adopt it fastest. They’re the ones who build the right foundation first — and find a partner who can help them get there without building a data science department from scratch.

Turning Missed Moments into Meaningful Connections in Community Banking

Article

Turning Missed Moments into Meaningful Connections:

How AI Drives Deposit Growth by Amplifying the Human Touch in Community Banking

Community banks and credit unions have always had a competitive edge: deep, trusted relationships with their customers and members. But in today’s environment, where digital expectations meet lean staffing and fragmented systems, even these institutions face a new kind of challenge.

Large banks are investing billions in AI to replicate what community banks do naturally — build relationships. According to Citibank, 93% of financial institutions expect AI to improve profits within five years, potentially unlocking $170 billion in industry-wide gains by 2028.

Yet the real issue facing community-based financial institutions isn’t just technology. It’s a quiet acceptance of the limits of human capacity — and the tolerance of inefficiency.

The Core Challenge: Banking Has Normalized Missed Opportunities

Most community financial institutions today have accepted that front-line staff can only do so much. Customer-facing personnel like branch managers, private bankers, and relationship bankers are responsible for hundreds, sometimes thousands, of customer relationships. With each client holding multiple accounts and generating thousands of transactions, it’s become operationally impossible to deliver the kind of proactive, personalized service that defines the brand of community banking. Without the tools to monitor every customer’s needs in a timely manner, they’re often limited to engaging only with the individuals who walk into the branch or proactively reach out to the bank or credit union.

The Result: A Culture of Firefighting

A customer quietly transfers funds to a competitor — and no one follows up.

A member switches jobs, prompting financial changes that go unnoticed due

to a lack of timely alerts.

A well-connected team member at a large local employer with referral potential is never identified as an influencer.

These moments aren’t missed due to lack of care or intention. They’re missed because banks and credit unions have had to accept the limits of their current staffing models and tools. Hiring enough employees to cover every opportunity would be cost-prohibitive. So, institutions settle for staffing formulas that prioritize coverage

over connection.

But what if you didn’t have to choose?

The Opportunity: Use AI to Scale Personal Service Without Scaling Headcount

That’s where Aunalytics comes in. Their solutions enable front-line staff to engage with all of their customers — not just those who raise their hands — by surfacing key activity signals and recommending the right time and message to connect. It empowers every banker to be in the right place, at the right time, which ultimately can lead to a net increase in core deposits. Rather than accepting that proactive service is too expensive, Aunalytics uses AI to unlock it at scale. It analyzes transactional and CRM data to uncover key relationship signals and delivers them directly to the banker or credit union professional. No combing through dashboards. No digging. Just timely, actionable insights tailored to each role.

Now, community-based financial institutions can identify critical relationship moments before they’re lost — retaining deposits, strengthening loyalty, and generating new business without increasing headcount.

Furthermore, Aunalytics goes beyond delivering a software solution by offering a strategic partnership that includes hands-on guidance and deep industry expertise. Every engagement includes a dedicated team of data engineers and analytics experts who guide implementation and support long-term success. This hands-on approach ensures institutions are not left to interpret or operationalize AI insights on their own.

The Critical First Step: An Intelligent Data Warehouse

The most important component of all AI systems is the quality and structure of the data itself, and the data model referenced to generate answers and perform humanlike tasks. Without a solid data foundation, AI efforts often struggle with fragmented, inconsistent, or incomplete data, limiting their effectiveness and scalability. Therefore, the first step is to create a reliable knowledge base to serve as the source of truth. In order to facilitate impeccable accuracy and traceability, Aunalytics has developed an Intelligent Data Warehouse and data model specific to community-based financial institutions to set their data and analytics initiatives up for success.

Auna: Insights That Find You

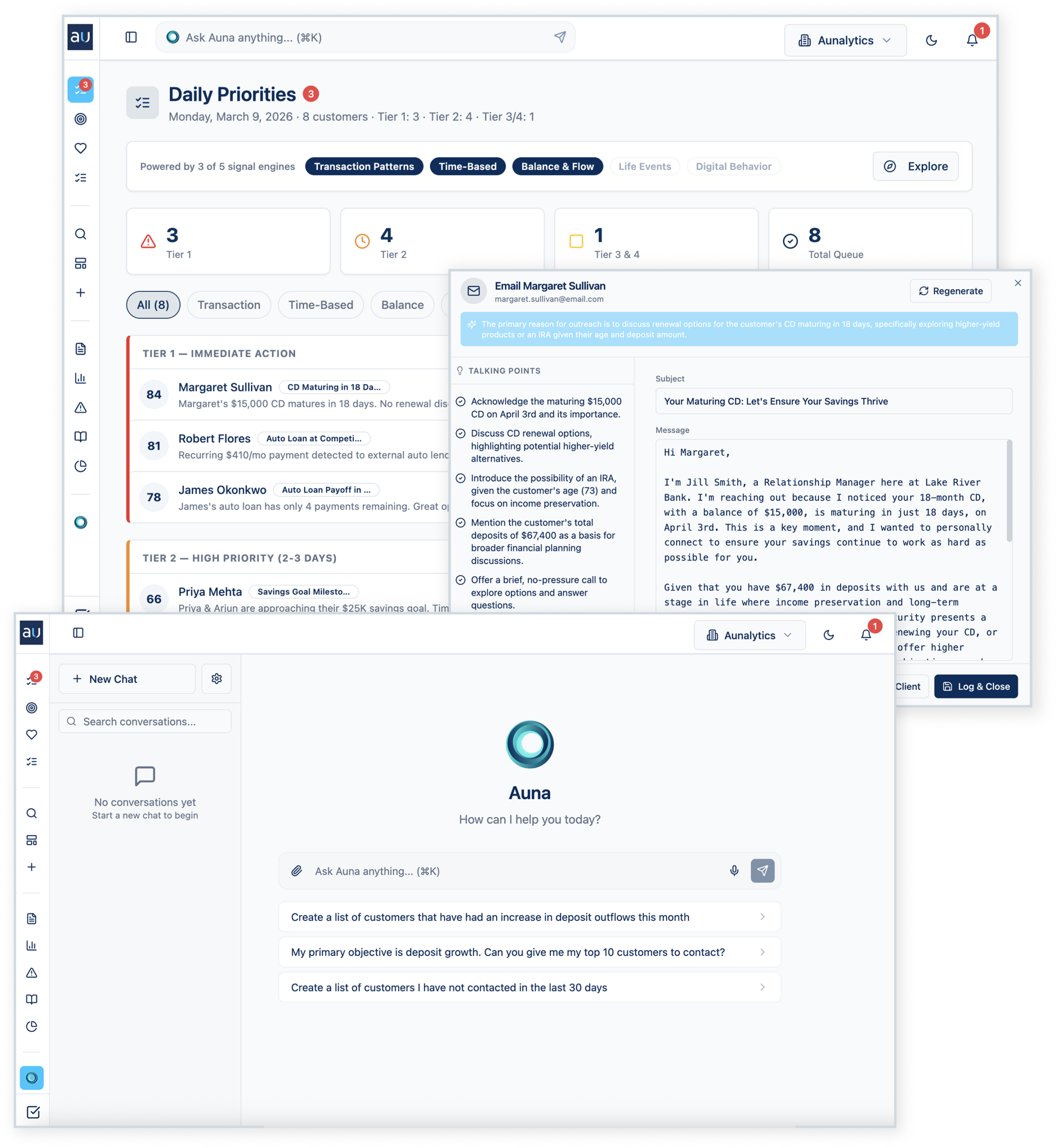

Auna is designed to help mid-sized financial institutions do work that drives growth. This approach shifts institutions from reactive responders into proactive relationship-builders, without requiring more people or more hours. Some of its main components are:

Daily Priorities: Instead of relationship managers pulling reports or digging through their email, Auna scans thousands of transactions from the last 24 hours, cross-references them against months of trend data, runs them against your institution’s playbook, and surfaces the five things you need to do today.

Personalized Outreach: Auna not only surfaces who should be contacted and when, but it takes it a step further and generates a personalized outreach message on the spot.

Conversational Chat: A private, natural language interface that allows any staff member to query near real-time data — no technical expertise required.

Examples in Action

- Retention: A high-value client moves a large sum to a competitor. Auna detects the transaction and prompts immediate outreach.

- Engagement: A shift in direct deposits signals a life transition. Staff receive an alert to check in and support the customer.

- Acquisition: A potential advocate is identified based on network or employer data, prompting the launch of a referral playbook.

Designed for Action, Not Analysis

Traditional BI tools often lead to “dashboard fatigue,” where the sheer abundance of data fails to drive business outcomes and the analytics are underused or overlooked. Auna elevates the focus from analysis to action. By surfacing just the insights that matter, right when they matter, bankers can spend precious time on relationships, not reporting. Even a few hours saved per week per employee compounds into hundreds of hours redirected to higher value activity across the institution.

Unlike dashboards that sit unused, Auna’s notifications are consistently read and acted upon. And the natural language chat feature ensures no question is too complex or too technical to answer.

A Modern Strategy for a Human-Centered Mission

Community financial institutions shouldn’t be forced to choose between digital efficiency and human connection. With Auna, they can have both. AI becomes an extension of their relationship model — empowering staff to drive growth by acting on what matters, when it matters, at a scale previously impossible. Because in a world of automation, relationships still win — and now, they can win at scale.

Banking Forward: Analytics Trends in Financial Services

Banking Forward:

Analytics Trends in Financial Services

In the world of financial services, staying ahead of competition means embracing analytics trends that enhance customer and member experiences and operational efficiency. As technology continues to reshape the industry, financial institutions are turning to advanced analytics solutions to gain insights on customer and member behaviors.

Higher Customer and Member Engagement through Online and Mobile Services

Improving the online and mobile experiences is at the forefront of modern banking strategies. Institutions are not only investing in robust mobile banking apps but also leveraging app data to gain deep insights into customer or member behavior. By analyzing transaction patterns, engagement metrics, and user feedback, banks can uncover valuable insights that inform strategic decisions and improve service offerings. This increased access to mobile services significantly enhances the customer and member experience by providing convenient access to financial information anytime, anywhere.

It’s important to note that improved mobile services play a crucial role in shaping personalized experiences, which have become a cornerstone of customer engagement in the banking industry. Through advanced analytics, banks can decipher intricate client data to understand their preferences, goals, and financial behaviors. This allows them to create tailored advice and personalized financial plans on a large scale. Detailed client profiles allow banks to anticipate needs and offer relevant products and services proactively, thereby enhancing customer satisfaction and loyalty.

Highly Personalized Advising

Advising Services, like personalized experiences, is another solution that ensures each client receives tailored assistance aligned with their specific needs. Advising Services have evolved significantly with the integration of customer relationship management (CRM) technology. By using CRM tools, banks can compile comprehensive customer profiles enriched with transaction history, communication preferences, and financial goals. This wealth of data allows financial advisors to deliver customized guidance that addresses each customer’s unique circumstances and aspirations. Such personalized advisory services foster stronger client relationships, driving loyalty and retention in a competitive market.

Enhanced Customer Service through AI-Powered Chatbots

Similarly, AI (Artificial Intelligence) is revolutionizing customer interactions within the banking sector and how they might seek out help. AI-powered chatbots are being deployed to handle routine inquiries and provide instant assistance, reducing wait times and enhancing customer satisfaction. These chatbots are integrated seamlessly into banking platforms, offering users real-time support and guidance. Moreover, AI-driven virtual assistants are being used to deliver personalized money management tips, empowering customers and members with actionable insights to make informed financial decisions.

Open Banking Initiatives

And while AI is implemented to assist clients, open banking ensures that clients retain ultimate control over their data. Open Banking represents a new era of connectivity and collaboration in financial services. By securely sharing customer information through APIs (Application Programming Interfaces), banks can build partnerships with third-party applications and services. This integration allows for enhanced functionalities such as aggregated financial insights, streamlined payment processes, and personalized financial recommendations.

Predicting and Preventing Fraud and Cyberthreats

Finally, with the increase of cyberthreats and ransomware, cybersecurity and fraud detection continue to trend as well. Effectively identifying and mitigating malicious threats calls for strategic planning and investments in tools and infrastructure. Investing in cybersecurity further enhances customer and stakeholder trust by committing to protecting their data and assets.

In conclusion, the banking and credit union sectors are embracing advanced analytics trends to enhance customer experiences, streamline operations, and drive sustainable growth. By leveraging technologies like AI, CRM, and open banking principles, institutions can deliver personalized services that cater to individual needs and preferences effectively. Embracing these trends not only positions banks as industry leaders but also ensures they remain relevant and responsive to evolving customer expectations in a digitally-driven world.

At Aunalytics, we are committed to empowering community banks and credit unions with cutting-edge solutions that leverage these trends. By partnering with us, community banks and credit unions can optimize their operations, strengthen customer and member relationships, and prevent cyberattacks and fraud events that can erode consumer trust. We believe in supporting our clients to ensure that they remain at the forefront of the financial services sector.

Becoming More Customer-Centric—How Community Banks and Credit Unions Can Cultivate This Mindset and Act on It

Personal, white glove service has always been a competitive advantage for community banks and credit unions. Therefore, a customer-centric mindset is vital. While a customer may be just another number at a large, national bank, community-based financial organizations can get to know people on a more personal level—and they may in turn feel a larger sense of connection and loyalty to a bank or credit union that has a history within the community.

But, as banking moves to be more digitally-focused, a familiar, friendly face at the bank counter is not enough, especially as younger generations embrace the convenience of online and mobile banking. Customer touch points are increasingly digital—which isn’t necessarily a bad thing. Financial institutions now have a wealth of data about each individual. Large, national banks are already using this to their advantage.

Many large financial institutions have invested billions in technology, including data and AI-based solutions that allow them to fully embrace customer centricity in their business practice. This allows them to foster relationships based heavily on digital interactions.

But without ample resources that can be focused on developing data-backed solutions, how can a smaller, community-based institution compete?

Adopting a Customer-First Mindset

While a focus on the customer or member is the bread and butter of most community banks and credit unions, there is always room for improvement. While customer centricity is a sought after ideal, only about 9% of organizations have achieved this goal. This can make it a competitive differentiator for organizations who manage to fully embrace this mindset. To become a truly customer-centric organization, it’s not enough to provide a high level of customer service. It requires customer centricity to be embedded in the organization’s DNA and across all functional areas of the financial institution.

A customer’s interaction with an organization goes beyond the tellers at the branch, or a mobile app’s user interface (though these are each vitally important elements!) There are some questions to consider when evaluating whether an organization is truly putting the customer first:

- Are your products and services what your customers really want and need?

- Are recommendations and advice being tailored to each unique individual?

- Are customers experiencing seamless interactions across all touchpoints?

- Are you using direct feedback and data to inform decision-making?

- Are you able to provide customers with “unexpected value,” beyond what they would normally expect from their financial institution?

In order to reach these lofty goals, organizations must first get buy-in across the organization and actively work to shift goals and mindsets.

Embracing The Power of Data and AI

Once a bank or credit union has determined that it is on its way to cultivating a customer-centric mindset, it is time to start taking action. One of the most powerful ways to become more customer-centric is to rely on insights from data. But the first step is to organize data into a 360-degree view of each customer—breaking down data silos in order to capture the entire customer journey.

Once data has been aggregated, cleansed, and organized around each customer, it can be used to make data-driven decisions, personalize the customer journey, and increase the effectiveness of marketing campaigns, and optimize operations. With the power of AI and predictive analytics, organizations can:

- Enhance digital interactions with chatbots;

- Enact offer relevant product suggestions;

- Determine which customers or members are most likely to churn;

- Identify potential new customers who look the most like their current best customers;

- Optimize loyalty programs to increase customer satisfaction; and more.

Where To Start?

If all of this sounds like a lofty goal, that is because it is. This undertaking can be a huge challenge for most midsized banks and credit unions. In many cases, it could take several months—or even years—to get to this point. That is why many organizations are looking outside their own walls to work with experienced partners to guide them through the process along with pre-built technology solutions that can reduce the time to implementation.

To meet the unique challenges of community banks and credit unions, Aunalytics has developed the Intelligent Data Warehouse—an end-to-end data and analytics platform using AI and machine learning to enrich a bank or credit union’s existing data and create a customer-centric view. This ultimately allows midsized financial institutions to more effectively identify and deliver new services and solutions so they can increase wallet share and better compete with large financial institutions.

Organizations Shift to Cloud-Based Analytics and IT Platforms

The growth rates of cloud-based IT solutions in the areas of analytics and artificial intelligence have been substantial in recent years. The increasing volume of data and the need for faster, more accurate insights have driven organizations to adopt cloud-based analytics solutions at a rapid pace. This has resulted in the growth of cloud-based data warehousing, business intelligence, and big data analytics solutions.

Similarly, the growth of artificial intelligence has been driven by the cloud, as it allows organizations to access powerful AI algorithms and training data without having to invest in expensive hardware. The cloud has also made it possible for organizations to scale AI solutions quickly and easily, leading to an increase in the adoption of cloud-based machine learning and deep learning solutions. These trends are expected to continue as organizations look to leverage the power of AI and analytics to gain a competitive edge in the market.

This growth in cloud-based analytics and AI has been driven by the larger business adoption of cloud IT because of its numerous benefits such as increased flexibility, scalability, and cost savings. Cloud technology allows companies to access their data and applications from anywhere, reducing the need for physical infrastructure and freeing up resources for other areas of the business. This shift towards cloud computing has also improved disaster recovery and business continuity, as data can be stored and accessed remotely. Additionally, with the rise of cloud-based solutions, businesses have been able to access advanced technologies and services without having to invest in expensive hardware and software. This has resulted in increased competitiveness, innovation and better overall business performance.

APIs add efficiency and flexibility to cloud environments

The power behind the most widely adopted cloud platforms are APIs (Application Programming Interfaces), which play a crucial role as they allow different software systems to communicate with each other and access data from the cloud. This has enabled organizations to build custom solutions and integrate disparate systems seamlessly, making the use of cloud technology much more efficient and flexible.

APIs also allow for automation and streamlining of processes, reducing manual errors and freeing up time for more valuable tasks. APIs make it possible to add new functionality and services to existing systems, allowing for continuous improvement and innovation. In essence, APIs provide a bridge between the cloud and an organization’s systems, enabling organizations to harness the full potential of cloud computing and drive digital transformation.

Analytics moves to the cloud

In terms of business outcomes, cloud-based analytics allow businesses to access and process large amounts of data in real-time, regardless of the size or location of their operations. This enables organizations to make informed decisions quickly and respond to changing market conditions with agility. Secondly, these solutions are much more cost-effective, as businesses only pay for what they use and do not have to invest in expensive hardware or IT infrastructure. The cloud provides businesses with access to a wide range of advanced analytics tools and technologies, enabling them to gain insights from their data in new and innovative ways. These solutions are highly secure and reliable when they are managed by experienced cloud service providers who ensure that data is protected and the solution is always available. Overall, they are considered to be a better choice for businesses because of their scalability, flexibility, cost-effectiveness, and secure approach to data analysis.

Likewise, cloud-based AI or AI as a Service (AIaaS) provides organizations with access to deep insights without having to invest in expensive experts or the necessary hardware and software to implement such solutions. This makes it easier for organizations to deploy and scale AI solutions as they only pay for what they use and do not have to invest in maintaining their own infrastructure. Furthermore, these solutions are more flexible and can be customized to meet specific business requirements, enabling organizations to generate valuable insights that help them to differentiate from their competitors. Finally, cloud-based AI makes it possible for organizations to collaborate and share AI models, allowing them to leverage the collective expertise of their partners, customers, and employees to create better solutions. In short, it is a high-value choice for businesses as it provides a more accessible, scalable, affordable, and collaborative approach to artificial intelligence.

Moving to the cloud accelerates digital transformation

Leading research and advisory firm Gartner reported that “Cloud migration is not stopping, IaaS will naturally continue to grow as businesses accelerate IT modernization initiatives to minimize risk and optimize costs. Moving operations to the cloud also reduces capital expenditures by extending cash outlays over a subscription term, a key benefit in an environment where cash may be critical to maintain operations.”

Aunalytics provides a highly redundant and scalable cloud infrastructure that enables midsized businesses to reap the benefits of the cloud at a reasonable cost. The Aunalytics Cloud provides a wide range of solutions—including cloud storage, backup and disaster recovery, application hosting, advanced analytics, and AI. Moving from on-premises computing to a cloud environment is a key step in an organization’s digital transformation.

Investment in Artificial Intelligence is Vital for Banks and Credit Unions

Has your bank or credit union made investments in artificial intelligence yet?

Advances in artificial intelligence (AI), and the promise it holds for the future, have been making news all year. And it’s no wonder that financial institutions are taking notice—a recent survey from the Economist Intelligence Unit found that 77% of bankers believe that unlocking value from AI will be the differentiator between winning and losing banks. Yet, many institutions are falling behind in AI maturity.

Despite its promise, making a large investment in artificial intelligence may seem risky to many midsized financial institutions. Hiring talent, developing a data management and analytics strategy, building a data platform, and creating AI models can be both time- and resource-intensive. Banks and credit unions want to ensure that the efforts spent to get an AI program off the ground will yield a high ROI, especially in times of economic uncertainty. Yet, failure to innovate and make progress toward digital transformation is not always an option in the highly competitive landscape.

Financial institutions find many uses for AI technologies

Thankfully, an investment in artificial intelligence can improve many processes across an institution. AI can optimize both time- and resource-intensive tasks, decrease risk, and increase revenue by improving the customer experience. For instance, by applying AI and machine learning algorithms to transactional data, banks and credit unions can gain insights into customers or members’ habits and preferences. Some use cases include:

- Detecting and preventing fraud

- Identifying loan default risk at the time of application

- Predicting customer churn

- Winning back business by discovering customer payments going to competitors, and subsequently making a more attractive offer

- Predicting the next best product for each customer then targeting them with the right product at the right time

- Calculating customer value scores in order to better allocate resources to target more valuable customers

Don’t get left behind

Large banks are already utilizing artificial intelligence use cases at scale. In a recent letter to shareholders, Jamie Dimon, Chief Executive Officer of JPMorgan Chase wrote, “Artificial intelligence (AI) is an extraordinary and groundbreaking technology. AI and the raw material that feeds it, data, will be critical to our company’s future success—the importance of implementing new technologies simply cannot be overstated.”

Because of this focus, his company has made tremendous investments in AI. They currently have over 300 AI use cases in production, and employ almost 3,000 people in data management, data science, and AI-research-related roles. This underscores how vital these new technologies are to success in the future.

Unfortunately, not every institution has access to talent and technology at the scale of JPMorgan Chase. That’s why Aunaytics has developed a cloud-based data and analytics platform to provide data management, advanced reporting, and predictive AI and machine learning solutions for midsized community banks and credit unions.

Auna, the AI Agent for Financial Institutions, allows institutions to learn more about their customers and members in order to provide a better overall experience—which in turn reduces risk, increases wallet share, and reduces expenses.

The Truth About Artificial Intelligence in Business

Is the existence of Skynet imminent or is that simply a sci-fi trope? In this brief video, Dr. David Cieslak, Chief Data Scientist at Aunalytics, talks about the capabilities of Artificial Intelligence in business, some potential concerns with AI, and where the technology is headed in the future.

While there exists a broad range of applications for AI, in the business world, this technology has the potential to drastically change how we understand our customers and how we use our data to interact with them. Once created and trained with customer data, AI has the ability to quickly provide suggestions and insights that would otherwise be prohibitively difficult or even impossible to observe on your own.

David Cieslak, PhD, is the Chief Data Scientist at Aunalytics since its inception and leads its Innovation Lab in the development and delivery of complex algorithms designed to solve business problems in the manufacturing/supply chain, financial, healthcare, and media sectors. Prior to Aunalytics, Cieslak was on staff at the University of Notre Dame as part of the research faculty where he contributed on high value grants with both the federal government and Fortune 500 companies. He has published numerous articles in highly regarded journals, conferences, and workshops on the topics of Machine Learning, Data Mining, Knowledge Discovery, Artificial Intelligence, and Grid Computing.